You Never Give Me Your Money

The COP29 conference is floundering with the usual tussle between the Global South asking for financial support to green their energy systems and the Global North pleading poverty. This article looks at some radical solutions for this impasse.

Funding the Energy Transition in the Global South

1. Introduction

There’s a couple of lines in the eponymous Beatles song ‘You Never Give Me Your Money, You Only Give Me Your Funny Paper’. Paul McCartney probably wasn’t thinking about the dodgy agreements signed at climate conferences when he wrote the lyric, but he might have been. These lines neatly encapsulate the fiction, dutifully signed at recent climate conferences, that private-public partnerships will unlock billions to fund the Global South[i]’s decarbonisation.

An opportunity exists. Countries in the Global South are often blessed with excellent solar resources, villages remote from the grid that need decentralised power generation and a strong political desire to replace with fossil fuel imports with renewable energy. For instance, India aimed to install 40 GW of rooftop solar by 2022. It missed the goal by a mile.

What businesses in the Global South lack is affordable finance. A solar installer in the Global South borrows at a higher interest rate, for a shorter-duration loan than installers in the UK. Loans from the West in US dollars or euros have low headline rates but the repayment has to be in hard currency, and the installer has to insure against an adverse movement in exchange rates, cancelling the advantage of lower interest rates. Financiers call local currency borrowing melodramatically, but not inaccurately, the ‘original sin[ii]’ because the punishment, in the form of high interest rates, is far worse than having to repeat Hail Mary a few times. Such investment in low-carbon technology is set up to fail.

There is no shortage of capital globally This is despite the fact that hundreds of trillions of US dollars of funds slosh around in the Global North, institutional investors (pension funds and insurers) and banks’ balance sheets, rarely earning a return of more than 8 per cent[iii].

This report focusses on the challenge of attracting private capital to fund climate mitigation in Global South. This focus is deliberately narrower than ‘climate finance’ and is focussed on spending on renewable energy and energy efficiency that reduce greenhouse gas emissions. Some of the data sets include spending on adaptation, loss and damages and funding for other sustainable development goals (SDGs). These are also grossly underfunded but will always struggle to woo private capital because benefits are either non-market, risky or payments for previous wrongs rather than investments. This report focuses on private funding sources, supplementing the renewable developers’ own balance sheet. These include local and international financial institutions. There is also discussion about blended finance – where concessionary finance from development banks and philanthropies is used to leverage private finance.[iv]

Spoiler alert: this report argues that financing levels are too low and that current ideas won’t bridge the gap. Creating a fair and sustainable world means a vast, fast redeployment of resources from continuing to fund overconsumption in the Global North to fund low-carbon development in the Global South. Section 2 looks at the scale of investment needed, particularly by the energy sector. Section 3 assesses the adequacy of these sources. Section 4critically reviews current plans for expanding funding. Section 5 looks at what’s really stopping private finance flows. Section 6 sets out some tentative and radical policies aimed at bridging the investment gaps so the South can achieve SDG goals. Section 7 has some end thoughts.

2. The gap between need and availability

The Global South need an additional investment of $4 trillion annually[v] to meet its SDG. goals. UNCTAD’s new estimate (UNCTAD, 2023[vi]) of the investment the Global South needs to achieve SDG, is up from the $2.5 trillion annual estimate it made in 2015. This adds up to $28 trillion between now and 2030. These figures are necessarily broad-brush. It would be a mistake to assume all of this spending on SDGS is in line with the ecological management of the planet. Some projects – e.g. new road transport infrastructure – might have an adverse effect on climate mitigation. But for the sake of this article, let’s assume that it improves people’s lives.[vii]

Of this, $2.2 trillion must be invested annually in clean energy, representing 60 per cent of the funding gap. UNCTAD’s estimate is in line with the IEA–IFC’s (IEA/IFC, 2023) estimate of an additional $2 trillion investment in energy by the 2030s[viii].

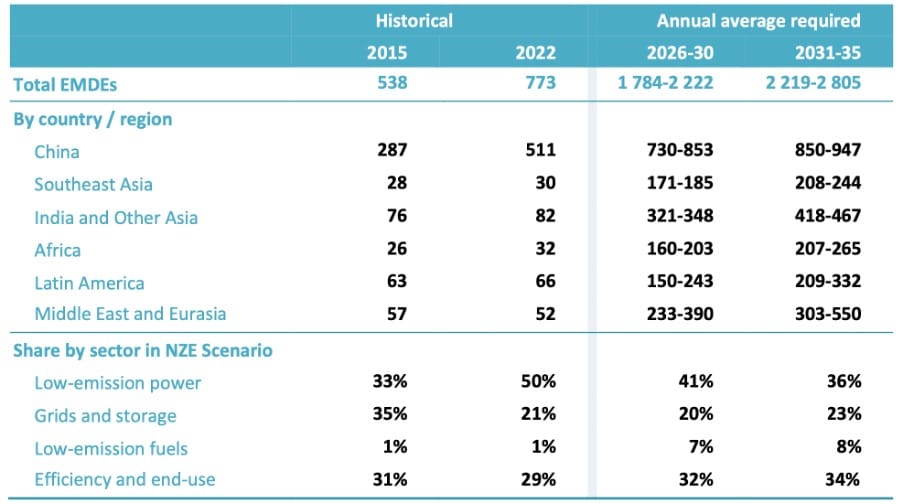

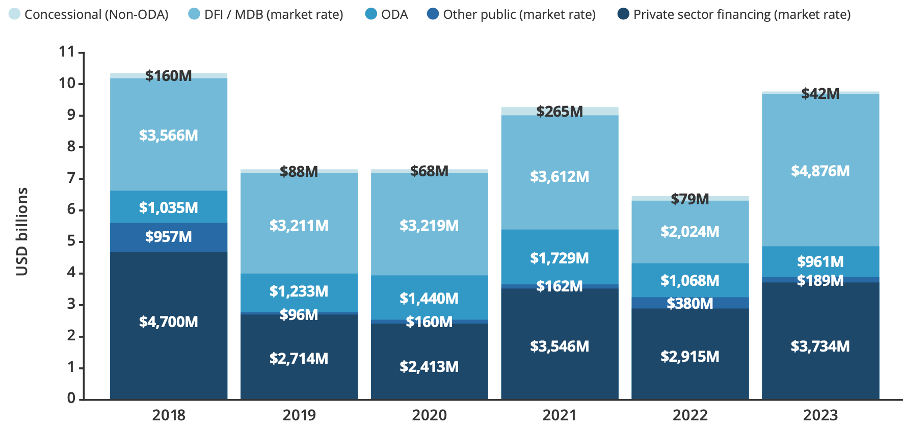

Only the Global North and China are spending enough on renewables. Exhibit 1 shows the vast differences in spending. China, with a population of 1.4 billion, spent $551 billion on clean energy in 2022. Countries in Africa, with a population of 1.15 billion, spent just $32 billion at a fifth of the rate of spending needed, despite dismally low per capita power generating capacity. By way of contrast, forty per cent of climate funding is spent by Global North countries with 10 per cent of the global population (Climate Policy Initiative – CPI, 2023). Ecologically sensitive development needs a vast increase in the quantum of money deployed and a switch away from fast-growing developing economies beloved by Global North investors to low-income countries in Africa and parts of Asia. China is the only Global South country where this transition is happening at pace. Current financial flows maintain the status quo of shuttling resources into already growing emerging markets, denying the poorest people the resources to meet their basic needs and live sustainably.

Exhibit 1: Annual Investment in Clean Energy Global South (EMDEs) to Align with SDGs (USD billion)

Source: International Energy Agency/IFC, 2023

3. Current sources of renewable energy finance

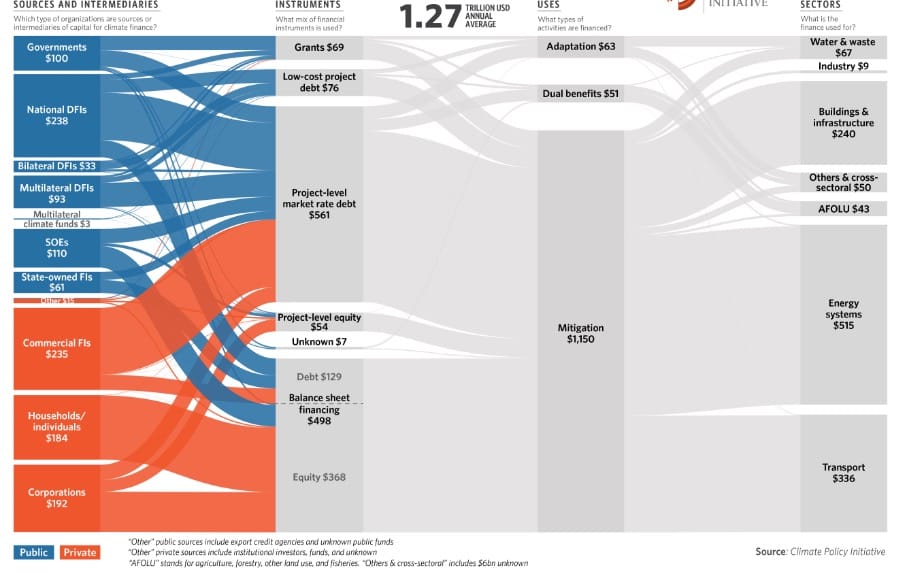

Most climate investment is raised locally from private sector banks and domestic public finance institutions. Only a tenth of it is capital flows to the South from the North. Exhibit 2 shows climate finance is almost equally raised from private sources ($625 billion) and public sources ($640 billion) (CPI, 2023). Private banks, national development finance institutions (like the UK’s National Wealth Fund), and corporations contribute about a quarter. Less than 10 per cent of total climate funding flows from the Global North to the Global South. Though $100 billion was promised under the Paris Agreement in 2016, despite efforts to grow flow the Global North is still only able to report $83.3 billion of annual deals. Oxfam calculates that two-thirds of this is in the form of lending at commercial interest rates[ix]. Only $21–$24 billion is real support through grants or interest rate subsidies, (Oxfam, 2023). This is far short of what was promised and piles on top of the South’s already unaffordable debts to the Global North and China (nowadays the largest creditor nation to other Global South countries).

Climate Adaptation is even more cash strapped than mitigation. Of the $1.27 trillion of climate finance, $1.15 billion is for mitigation. Very little is spent on investments to prepare countries for inevitable climate change (adaptation and resilience) or compensate them for damages they already suffer (loss and damage).

Exhibit 2: Landscape of climate finance in 2021/22

Source: Climate Policy Initiative, 2023[x]

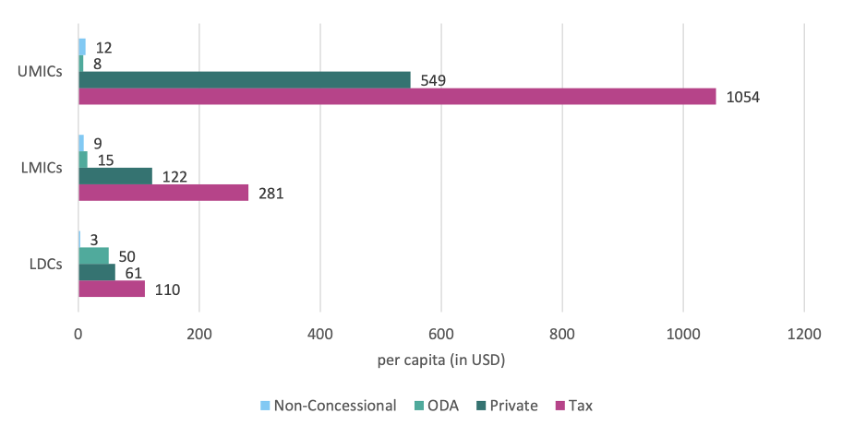

Richer Global South countries spend far more on SDGs than poorer ones relying on their own government and the private sector. Low-income South countries’ domestic financial base is inadequate, and international flows are insufficient to redress the shortfall. Exhibit 3 shows the level of investment in SDGs (wider than renewable energy) for different income levels of the South. Least developed countries (LDC) neither raise money domestically from taxes nor from private sources. How about overseas aid? In 2022, Overseas Development Assistance from the North to the South amounted to $210 billion, around 0.37% of donor countries’ gross national income and far short of the 0.7% target. Already, aid budgets face overwhelming pressure from conflicts in Ukraine and Gaza. Can this be significantly expanded? Governments in high-income countries are already wrestling with large current account deficits and have eye-watering stocks of existing debt. Indeed, increasing flows from $50 to $1,500 per LDC’s inhabitant would cost $1 trillion per year, an unimaginable five-fold increase in aid flows. Increasing government transfers from the North to the South to this extent would require a massive restructuring of resources within the North. Many Global North governments are heavily indebted; wealth in the Global North is held by rich and middle-class people.

Exhibit 3: Financing of SDG investment by income level of investee country ($/capita)

UMIC – upper middle-income country; LMIC – lower middle-income country; LDC – least developed country

Source: Bill & Melinda Gates Foundation[xi]

Poorer countries’ economies are too small to raise funds locally and judged too uncreditworthy to borrow internationally. Exhibit 4 shows key economic and demographic differences between countries grouped by income band. 1. Low income and 2. Low Middle Income Countries account for half the world’s population but just 8% of global GDP. If a tenth of their GDPs were somehow invested in SDG, this would raise just $250 per capita in LMICs and a paltry $70 per capita in LDCs. The domestic economies do not generate large enough surpluses to finance their development. The last column gives the credit rating agency (CRA) Moody’s assessment of each government’s ability to pay back debts to bondholders. Countries in groups 1 and 2 are deemed poor credit risks. Projects in these countries would find borrowing money from commercial banks difficult no matter how spectacular the returns. Institutional investors would regard the country as ‘below investment grade’ as the country’s credit rating puts a ceiling on the creditworthiness of local companies. Most LDCs do not even have a credit rating since there is little possibility of borrowing commercially. Grants and concessionary finance are their only option for funding the transition.

Exhibit 4: Macro-differences between countries by World Bank development class

Country development class | Population (million) | GDP ($ tr) | Total debt ($ tr) | GDP $000 /capita | Example countries | Credit rating |

1. Low income | 678 | 463 | 18 | 0.7 | sub-Saharan Africa | Unrated, Caa |

2. Lower middle income | 3,190 | 8,103 | 409 | 2.5 | South Asia, Latin America | B – Baa3 |

3. Upper middle income | 2,813 | 30,120 | 28,816 | 10.7 | China, SE Asia, South America | B – A3 |

4. High income | 1,220 | 61,565 | 47,551 | 50.5 | OECD, Middle East | Ba – AAA |

World | 7,900 | 100,252 | 76,794 | 12.7 | | |

Source: authors’ calculations

This has nothing to do with the merits of the underlying projects or the borrowing company. CLP (a Hong Kong-based power company) sought funding for its Indian subsidiary (India is a Lower Middle income country) to refinance its wind farms. It accomplished this by issuing a ₹9 billion (USD60 million) bond with a coupon of 9.15%. This local currency issuance was still cheaper than raising an international currency bond, such was the adverse sentiment of global investors about lending to India at the time. When CLP raised a bond in Hong Kong (for investment in a gas-fired power station), it paid a coupon of just 2.15% since the Hong Kong dollar is pegged to the US dollar and trusted by international capital markets not to depreciate.

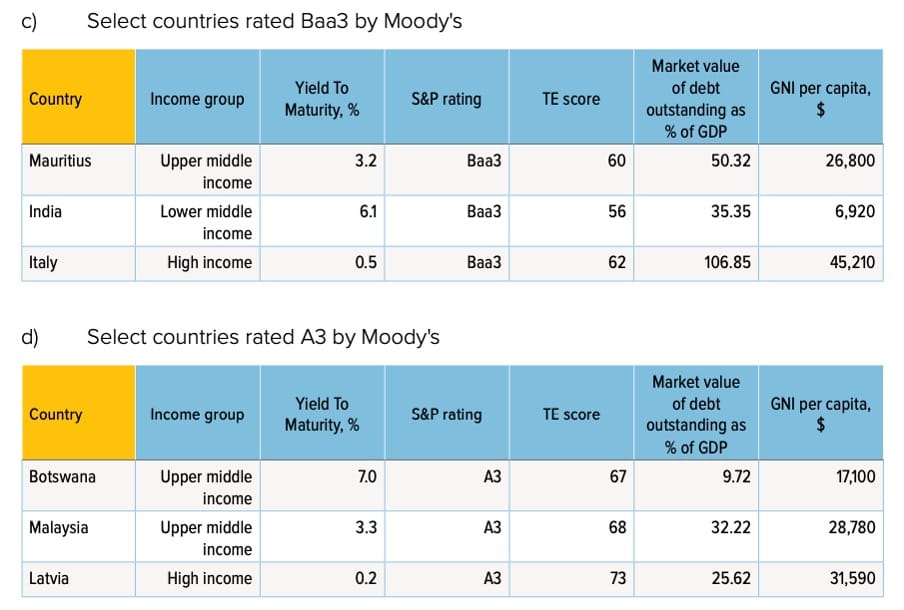

Projects are not judged on their own merits but tarred by national stereotypes. The returns for solar photovoltaic projects in Africa are spectacular because the alternative of diesel-generated power is expensive, and the continent is sunny. However, international finance is reluctant to invest in African countries, worried the currency might depreciate, fearful the courts will not honour contracts, and otherwise concerned by governments that are little understood or trusted by the Global North’s banks. Costs for countries with the same credit rating are ruinously expensive if they have the misfortune to be located in Asia or Africa rather than Europe see Exhibit 5.

Exhibit 5: Yields for investors in bonds from different countries with the same Moody’s credit rating

Source: UNDP, 2023[xii]

Only predatory capitalists offer low-income countries funds None of the above arguments are binding constraints.Countries, when it suits them, will disregard credit ratings or any anxiety about good governance or political tampering. The Democratic Republic of Congo (DRC) has a terrible credit rating and a history of poor governance. Yet, it can attract foreign direct investment from China to exploit its rich mineral resources for strategic control of the raw materials used by EV batteries. Chinese companies now own and control 15 out of 19 of DRC’s best copper and cobalt mines, enjoy tax-exempt status and face little accountability from the DRC government (Gregory and Milas, 2024)[xiii].

4. Mainstream consensus for funding SDGS in the Global South

There is little appetite for increasing aid budgets from advanced economies, and so private finance has been cast to plug the gap. The development community is well aware of the need to massively scale up funding in the poorer half of the world, and countless reports have been written about the challenges. The broad parameters of the debate are that:

a) There is a reluctance for Global North governments to greatly increase how much they contribute to SDG investment directly as grants or soft loans.

b) Political effort is being expended on redirecting the vast pool of savings managed by institutional investors (pension funds and insurers) and banks from OECD countries, through efforts like the Glasgow Financial Alliance for Net Zero (GFANZ) formed during COP26.

c) Multilateral development banks (MDBs) are being tasked to use their resources and expertise to help make private sector investments less risky through due diligence work and by using their balance sheets to bear some of the risks. This combination of public–private financing is termed blended finance.

Blended finance is being promoted as the mechanism for converting “billions” to “trillions”. Blended finance consists of several mechanisms which use public funds to de-risk projects and loans to the Global South. Its beauty is that a relatively small amount of government spending from cash-strapped Global North countries is used to lever in private funds. A plethora of consultants and think tanks have written reports on the topic (Better Finance Taskforce, Convergence, OECD-DAC). MDBs are presented as important catalysts and conduits because of their experience in lending to the South, assessing and managing projects, and their financial credibility. They also have the option of funding on their own balance sheet and borrowing money cheaply on capital markets to refinance the deal. Discussions about blended finance are often discussed in the same breath as overhauling the international financial architecture, shifting MDBs’ goal from pure lending to facilitating lending by others.

The G20 grouping which includes Global North and South countries also calls on blended finance India, during its G20 presidency in 2023, commissioned an expert report to advise on how to plug the gaps in SDG funding. It argued an annual increase of $260 billion in MDBs’ budgets could leverage $500 billion extra private finance. Domestic capital markets would unlock $2 trillion of within-country funding.

….as do signatories to the climate change agreement The climate COP process has convened a high-level expert group on climate finance to help deliver the Paris Agreement. (COP IHLEG, 2023)vi This group reaches similar conclusions to the G20 group, arguing for a five-fold increase in concessional finance, the loosening of MDBs’ conservative approach to using their balance sheets to promote lending, a better use of domestic tax revenue by the Global South, and the removal of harmful subsidies (many developing economies continue to subsidise fossil fuel production and consumption), receiving countries to better organise their investment projects into a pipeline. Actions are also proposed to remedy some of the acute budget issues caused by the pandemic.

These schemes aim to mobilise the necessary $3 trillion per year of finance, with $500 billion per year of this coming from the Global North’s private finance and the same amount through the MDBs. Many high-level reports repeat mantras exhorting development banks to up their game and use their balance sheets more creatively. At a conference, I attended, one senior MDB official lamented that he and his colleagues are under pressure to increase the amount of private finance they leverage.

But private finance is nearly absent from the discussion Interestingly, the delegates at the conference comprised NGOs and local and national officials. Is there much appetite for Western banks and insurers to invest in emerging markets? In typical climate finance events, private investors are conspicuous by their absence: a smattering of bankers, no asset managers nor asset owners.

Private finance flows are currently a fraction of necessary levels and there are significant cultural differences between private and public financiers. In the COP report only $17 billion in private finance is leveraged through the MDBs’ $80.6 billion for climate action in 2022. Private finance needs to scale up twenty-five-fold if it is to play the starring role being asked of it. Blended finance is difficult and time-consuming to negotiate. Public authorities and private banks have different objectives, and private finance is impatient with MDBs’ glacial internal processes. Most institutional investors are ignorant about developing economies[xiv] and the few with practical experience have entrenched (mis)perceptions about country risks, see a lack of bankable project pipelines (because they seek projects that have obtained clearance, are profitable and not too risky)[xv]. There are few examples of blending efficiently leveraging in institutional finance and many indications that private sector banks do not see as their job to finance SDGs or energy transitions. In closed meetings private sector bankers are critical of MDBs, finding the institutions slow to undertake transactions, bureaucratic and lost in a cacophony of political demands imposed by their shareholders. A development financier puts it well: “They talk about mobilization, but they don’t walk the talk,” the investor said. “Incentives have not changed at the deal-structure level.”

There has been little increase in the volume of blended finance over the last five years. Convergence’s database on blended finance transactions contains details of 1,100 deals worth $216 billion over the past ten years. Exhibit 5 from its most recent climate finance report records 45 deals worth $6 billion in 2022, lower than recent years because global interest rate hikes have reduced investors’ already-small appetites to take a punt on THE GLOBAL SOUTH. Deal numbers rose in 2023 but still not to pre-pandemic levels. Worryingly, only $3.7 billion of the $10 billion was genuine private sector funds, the rest was MDBS charging commercial interest rates and using their balance sheets to lend to projects. In 2023, only $3.72 billion of the $11.6 billion blended finance transactions were genuine private sector finance, a far cry from the trillions that need to be mobilised. The aggregate leverage rate was much less than 1. This is not a story of MDBs magically converting billions to trillions, but of billions to another billion. At the aggregate level concessional lending and development banks are the predominant provider of finance, not private finance, within blended finance deals.

Exhibit 6: Sources of financing to climate blended finance (excl. guarantees and insurance)

Source: Convergence database of blended finance deals

Recent, higher interest rates make lending to the Global South harder Post-pandemic inflation worries have caused interest rates to rise, the private sector’s willingness to lend has waned, as has the capacity of GLOBAL SOUTH COUNTRIEs to repay their mushrooming debt burdens.

5. What’s stopping private capital moving to the Global South despite the opportunities?

There are some specific blockages to funds moving South. Reforms to increase flows of private finance from the Global North to the Global South are not easy. They can be summarised as a) financial regulations, b) currency hedging costs and c) debt distress.

a) Financial regulations: Since the financial crisis, regulators have tightened regulations around banks (Basel IV) and insurance companies (EU’s Solvency II) to reduce their exposure to risky assets. Banks must set aside far more scarce capital if they lend to sectors or countries with poor credit ratings. Conversely, investing in government bonds or home loans with a low loan-to-value ratio is treated leniently. Thus, banks lend to the haves rather than the have-nots, perpetuating inequality within and between countries. Basel IV, will impose the regulators’ risk weights on different financial products, preventing banks from using their own judgements. Banks must argue with their central bank exceptions for blended finance deals and lending to pre-approved borrowers is easier! UK insurers, despite Brexit, are still following the EU’s Solvency II rules, which takes a dim view of investing in the Global South.

b) Currency hedging costs: though the US’s global power might be waning, there has been no scaling back of the dominance of the US dollar in development finance. To access global capital markets, Global South countries and their banks and companies issue debt in dollars; borrowers must pay back in dollars. Take it or leave it. Most borrowers leave it – since renewable electricity projects create revenue in local currency not dollars. Any depreciation in the local currency can swallow up the savings from lower interest rates borrowers in the West enjoy. In theory, banks offer products for borrowers to hedge their exposure to depreciation, but the fees are too high to be cost-effective.

c) Debt distress: the amount Africa spends on debt service is more than twice the amount of Overseas Development Assistance the continent receives. The situation worsened after the pandemic when inflation and interest rates rose. The pandemic was destabilising; many small, well-run countries like Sri Lanka and Fiji that depended on tourism suddenly saw their foreign income earnings collapse when international flights stopped. They borrowed from the IMF and now find themselves with unsustainable debt-to-GDP ratios. Sri Lanka’s debt soared from 80% to 120% of GDP between 2020 and 2022. While the US government, as the guarantor of the global reserve currency, gets away with huge external debts with impunity, lenders turned the screws on developing countries that try the same thing. Many countries have max-ed out their credit lines with the North.

Suggestions for massively scaling up Resolving these blocks is necessary but not sufficient. Private finance does not have much experience with lending to the Global South. Even if blocks issues are somehow removed, it doesn’t mean private finance will supply the South with affordable finance. ODI surveyed 35 of Europe’s largest pension funds and insurers and found that rules, risk appetites and habits meant they could double their investment in Global South to $120 billion in five years out of the $6.9 trillion assets under management[xvi].

Private finance relies on credit rating agencies (CRAs) to assess sovereign risk which then banks use to set the price of finance when lending. The process is a Milton Friedman-esque contest where CRAs judge countries by the fiscal-anorexia of their public spending. Exhibit 5 debt shows the debt servicing costs for African, Asian and European countries with the same credit rating – i.e. judged to have the same likelihood of defaulting. Australian pension fund managers, interviewed for a report by a green finance NGO, say they are interested in investing in the Global South but insist their funds should be fully compensated for the perceived risk. There is no inquiry as to why the South are automatically charged more.[xvii]

The Global North’s institutional investors invest close to home despite unremarkable returns. The current value of shares traded in global stock markets is around $109 trillion. The vast majority is in the Global North, (with the $22 trillion Chinese and India stock markets mainly used by domestic investors). The global bond market is $127 trillion, again the Global North borrowing from the Global North. Perhaps the largest pool of assets is the real estate market. The US’s real estate market is valued at $120 trillion, which includes $47 trillion value of residential properties. Yes, the assets owned in slow-growing OECD countries are vast, but their returns are modest. At the time of writing, investors in UK gilts get a yield of 4.5% on UK gilts, 2% above inflation. Before the recent interest rate hikes, they yielded less than 1%.

Institutional investors continue to buy assets in the Global North rather than take a punt on investing in (higher yielding) Global South through financial regulations, habit, and ignorance. A pension fund that has to provide teachers or doctors with a defined income in ten years looks for assets with the same payout profile that won’t go bust in the meantime or fall in value. Accountancy rules[xviii], mark-to-market rules and regulations[xix] compel them into buying gilts and low-risk bonds that provide a guaranteed but low income and value at redemption. However, as a consequence, money flows into existing assets like mortgages or backstops government deficits rather than real-world investments. This is bad for young people who cannot afford homes inflated in value by cheap money, and it is bad for global equality as the Western countries’ reluctance to raise taxes stimulates overconsumption by the current generation, at the expense of future generations saddled with debts – financial and ecological. It is also bad for the pensioners since the low-risk investments being incentivised provide lower returns over the long term and have contributed to the closure of defined benefit schemes!

6. Suggestions for massively scaling up funding for the energy transition funding in the Global South

Many countries will only transition their energy system with external help Many problems afflict the Global South: corrupt governments, poor education and health systems, massive wealth inequality, and religious and ethnic conflicts. But these have to be fixed domestically, and the North’s interference will be ineffective or cosmetic. The energy transition is different. The international community can make a difference since the energy transition, with the exception of larger countries like India and Brazil, relies on imported gear: panels, wind turbines, and Li-ion batteries. Global South countries need finance, especially foreign exchange. At present, China is the largest supplier of goods for this transition and through its Belt and Road Initiative and policy banks one of the largest financiers. The Export–Import Bank of China alone has lent out £0.7 trillion[xx], but it lends at commercial interest rates, has opaque and onerous financing terms and refuses to countenance debt forgiveness.[xxi]

What is needed is a totally different approach to financing the Global South’s energy transition while also reforming the Global North’s finance sectors so they focus on productive investments. The ideas presented below are unapologetically controversial and the intention is to think the unthinkable. This means addressing the fact that the rich extract more from the global commons than the poor, and that the North profits from this inequality at the expense of the South. Redress means redirecting cheap finance away from the already rich and towards the poor, sharing responsibility for macroeconomic risks with the lending countries (who likely as not caused them) and lastly removing the dollar’s unholy privilege as the global currency.

a) Increase and institutionalise transfers from the North to the South. This suggestion is to have a redistributive mechanism to transfer tax revenue from the North to the South just as regions within a country equalise per capita resources. This will institutionalise the rebalancing of income/wealth between countries rather than leaving it to the whim of donor countries to define their overseas development assistance level. The exact mechanism is not important for the purposes of this paper. Some that have been proposed include a 1.5% tax on wealth assets (inspired by Piketty[xxii]), on excessive national per capita carbon emissions (Raghuram Rajan[xxiii]), on individual carbon inequality (Kenner[xxiv]), or on financial transactions (Tobin Tax, or France’s financial transaction tax[xxv]), obliging banks to lend a share of their portfolio to the Global South like India’s Priority Sector lending regulations which provides finance for traditionally unbanked sectors[xxvi].

b) Provide grants and interest rate subsidies only to investments in compliance with the EU green taxonomy. These transfers to the Global South should have strings attached. This could include investments must be in projects that address climate mitigation and adaptation and have effective mechanisms to ensure funds reach their target use. Green or transition loan/bond standards using standards and principles set by the International Capital Markets Association and similar bodies build in such checks.

c) Tough capital control on illicit capital flows from South to North. A number of politicians and businesses in the Global South loot their countries, transferring their wealth to the North. This drains their country of foreign exchange and puts downward pressure on the exchange rate. UNCTAD have calculated that $88.6 billion are extracted from Africa through tax and commercial practices, illegal markets, theft and terrorism financing and corruption[xxvii]. This figure is half the gap in funding for SDGs. Regulations on banks in some Global North countries have done much to counter money laundering. But there are still too many loopholes and non-cooperating jurisdictions. But many advanced countries like Singapore and Luxembourg or territories like Delaware, Guernsey and Hong Kong continue to have banking secrecy laws aiding these movements.

d) More financial regulations on systemic risks, less on individual FIs or transactions. Financial regulation is focussed on safeguarding individual depositors. Since the Great Financial Crisis (GFC) It has since been extended to systemically important banks but in so doing has made banking too risk-averse and too reliant on backward-looking default rates. This tars individuals and entire countries as risky, denying credit to those who need it. Insurance funds operate under similar rules. Regulations need to be loosened to allow banks and MDBs lending to the Global South to use their own risk models. Private sector CRAs’ and accountants’ behaviours have a chilling effect on lending to new markets or new products.

e) Lenders should bear at least half of the currency risk. The use of hard currencies for most international capital market transactions is a major source of global inequity and just one facet of the outrageous privilege enjoyed by the dollar (also the currency for commodity markets, national currency reserves). It transfers the risk of devaluation wholly on to the borrower, greatly increasing the cost of finance. This privilege is despite China’s (a major international creditor nation) and India’s (with foreign reserves equivalent to its GDP) formidable economic size. Currency hedging can add 2–3% to the cost of debt and make long-dated loans impossible. To remedy this, international investors should purchase local currency bonds, and global North governments should bear half the costs of any unfavourable depreciation.

7. Some end thoughts

Global North governments’ and financial institutions’ immediate response to the suggestions above might be “Thanks, but no thanks. We like things as they are now.” How can winners from the current situation be persuaded to take action that hurts their (short-term) interests?

This is a challenging question to answer, as is evident in the recent climate COPs. The COP in Baku almost collapsed through the fundamental disagreements between countries with different and perhaps incompatible agendas. Those with fossil fuel reserves are trying to row back from restrictions being placed on their drilling, rich countries who are finessing mealy-mouthed text that avoids commitments to offer climate grants and developing countries, especially the Alliance of Small Island States, who want funding and technology to avert the existential risks they face.

But the chain of reasoning would first need to recognise the current situation is not in the interests of the Global North nor the South. Asset managers in the North need to invest in higher-yielding assets to pay for ageing populations’ pensions. Growth is fastest in middle-income countries. The world needs this growth to leapfrog from fossil fuels straight into renewables (and a circular materials flow, protection and restoration of biodiversity). Instead, well-meaning financial regulations’ risk-weightings and capital adequacy rules funnel Global North savings into housing bubbles, financial assets and funding government deficits instead of productive uses of savings.

Secondly, we need to recognise the Global South is not going to cut its emissions unless the North delivers on the climate finance that was promised to them in Copenhagen, then in the Paris Agreement, and expanded in Baku climate change COP. Many of the NDCs signed by the South state bluntly their cooperation is contingent on financial assistance from the richer northern countries. For instance, Philippines offers to reduce its projected emissions by 75% but only 2.71% of this is unconditional, the rest requires ‘enhanced access to climate finance, technology development and transfer’. Indonesia has similar conditional and unconditional reduction targets. India’s NDC target has the proviso “…with the help of transfer of technology and low-cost international finance…”

Starved of external funding, fast-growing Global South countries will reduce capital-hungry investment in renewables and continue to build less capital-intensive coal and gas generation, that will persist for decades and cost their consumers more in the long term. South Africa has issued a comprehensive plan of how it could close its coal plant and switch to renewables and bail out its near-bankrupt power utility Eskom (Iyer, K and P Vaze, 2024[xxviii]) with a cash injection of USD 100 billion. Indonesia and Vietnam have similar Just Energy Transition plans.

The second point is that stopping emissions is in the Global North’s interests since they are experiencing climate change already. In October 2024, Hurricane Milton is barrelling through Florida destroying property and infrastructure and leaving millions without power. Central Europe experienced abnormally heavy rainfall in September (Storm Boris) and its second warmest recorded September. Towards the end of October 2024, over 200 were killed in floods in Valencia, Spain in an unprecedented tragedy in a modern European country.

The third point is that the current ideas being discussed are rubbish. There have been scores of reports setting out the need for trillions of dollars of investment in the Global South. The Washington Consensus tells itself aid, development loans and private finance can somehow work synergistically and provide a market-led solution to SDG financing. Such a delusion repeated over and over, does not become true, but it can forestall genuine reforms.

The Global North’s efforts to supply climate finance is premised on deceit. It pretends that instead of government-to-government transfers, profit seeking financial institutions will spontaneously seek out higher yields in the Global South. This belief that without changing the fundamental rules of global financial flows, Western capital can aid development, make acceptable rates of return to private capital and make bankers feel warm inside has been proven false. See it, say it, sorted is not just an annoying meme. It is patently untrue. The less palatable truth is that the West needs to reign in profligate use of capital and be more generous in helping poor countries enhance their global competitiveness by transferring technologies and providing markets for goods like vehicles which India can now produce at a fraction of the cost of Western producers. It means a reduction in wealth and consumption in the North so the global commons can be shared more equally.

It is hard to remember how readily Western banks lent to developing countries in the 1970s when they were flush with petrodollars. Ever since the GFC, the tide has reversed, and ‘prudential’ banking practices starve risky projects of finance, instead lending to those with security in their homes and businesses. This conceptualisation of ‘prudential’ is mean and myopic. The world operates as a system, and there will be consequences of denying poor countries their opportunity to enhance their lives. Starved of development opportunities, Global South migration from Africa and Latin America will only increase, especially as climate change makes the tropical latitudes less habitable.

The Beatles song “Mean Mr Mustard” has the lines Keeps a ten-bob note up his nose, Such a mean old man. John Lennon probably didn’t have the global North in mind when he wrote those lyrics, but he might have.

Acknowledgements:

Prashant Vaze is an India-based British economist who works on climate finance. Thanks for comments from Emma Dawnay, Jonathan Essex, Peter Newell, Damla Dogan Altinoren, Maria Urquiza and Pritam Singh.

Peter Sims

Peter SimsRelated Publication

[i] The Global South is used as shorthand for the 160 countries the World Bank classifies as low-income and middle income; and which financial markets call Emerging Markets and Developing Economies. The Global North is used to describe what the World Bank called Advanced Economies. See https://www.imf.org/en/Publications/WEO/weo-database/2023/April/groups-and-aggregates

[ii] https://en.wikipedia.org/wiki/Original_sin_(economics)

[iii] 8%–9% by Nest Pensions (the UK’s largest pension provider by customer numbers)

[iv] Definitions of blended finance can be found in Convergence’s latest report

[v] The NHS budget in 2023/24 was around $217 billion, so the Global South SDG needs are twenty times greater

[vi] UNCTAD (July 2023) “World Investment Report 2023”

[vii] Sims, Eastoe and Essex (2021) “Global Public Investment requirements for Zero Carbon”

[viii] IEA & IFC (2023) “Scaling up Private Finance for Clean Energy in Emerging and Developing Economies”

[ix] Oxfam (2023) “Climate Finance Shadow Report 2023”

[x] Climate Policy Initiative (2023) “Global Landscape of Climate Finance 2023”

[xi] Bill & Melinda Gates Foundation, June 2023 “Climate and Development Finance: A transition framework for all”

[xii] UNDP (2023) “Reducing the Cost of Finance for Africa”

[xiii] Gregory F & P Milas (2024) “China in the Democratic Republic of the Congo: A New Dynamic in Critical Mineral Procurement” Strategic Studies Institute US Army.

[xv] PWC “Scaling up Blended Finance”

[xvi] Attridge, S., Getzel, B. and Gregory, N. (2024) “Trillions or billions? Reassessing the potential for European institutional investment in emerging markets and developing economies.” ODI Working Paper. London: ODI

[xvii] IGCC (2023) “Mobilising climate investment in emerging markets – opportunities for Australian pension funds”

[xviii] https://www.plsa.co.uk/portals/0/Documents/0190_%20Accounting_for_PensionsL.pdf

[xx] Financial Highlight on page 7. Total assets of RMB 6.3 tr

[xxi] https://www.orfonline.org/research/chinas-belt-and-road-initiative-in-the-energy-sector

[xxv] https://en.wikipedia.org/wiki/Financial_transaction_tax

[xxvi] Priority Sector Lending regulation in India

[xxvii] https://unctad.org/system/files/official-document/aldcafrica2020_en.pdf

[xxviii] Iyer K & P. Vaze, “Landscape of Public Finance and the Role of Public Finance”

{kind=link}